Ever wondered how one clear plan can change the way you buy a home or manage money?

Welcome to TipsLends.com, where we offer practical tools and expert-led content that help make complex topics easier. We focus on real estate, mortgages, loans, and personal finance so you can act with confidence.

Use our site to learn step-by-step mortgage basics, compare lenders, and plan a realistic budget. Our guides show how to track credit, weigh down payment options, and factor closing costs so you can make sound financial decisions.

Explore our resources for clear checklists, market insights, and actionable tips. For a detailed walkthrough of the home buying process, see this home buying guide.

Welcome to Your Trusted Guide to Smarter Financial Decisions

in professional business attire, engaged in an animated discussion around a table filled with charts and financial documents. The middle ground features a large whiteboard with colorful diagrams illustrating budgeting, investment strategies, and saving methods. The background includes bookshelves filled with finance-related books and a large window showing a city skyline, filled with soft, natural light. The overall mood is collaborative and inspiring, with bright, warm lighting enhancing a sense of professionalism and optimism about financial empowerment. Capture the image at eye level to create an intimate and engaging atmosphere.")

A strong grasp of money basics gives you more control over major life decisions. The National Financial Educators Council defines financial literacy as the ability to understand the use of money as it applies to personal finance.

At TipsLends, our mission is simple: provide clear, practical content that helps you make better personal finance choices. We break complex topics into easy steps so you can plan, save, and invest with confidence.

- Understand how money works in your daily life and long-term plans.

- Build skills that make sound decisions and boost financial stability.

- Navigate banking, credit, loans, and investments with less stress.

Every guide focuses on core literacy concepts so you can handle economic challenges and grow wealth wisely. For a step-by-step home buying primer, check this guide for beginners.

Understanding the Core Principles of Financial Literacy

Learning core money skills helps you handle daily accounts and plan for future life events. These basics form a framework you can use when facing loans, savings goals, or big purchases.

The five key principles are simple and practical. Mastering them gives you control over personal finance and clear steps for good financial decisions.

- Earning: Track income streams and understand how pay, taxes, and benefits affect take-home pay.

- Saving: Build an emergency fund, set savings goals, and automate deposits to grow wealth steadily.

- Borrowing: Know loan terms, debt limits, and how interest changes the cost of a home, car, or student loans.

- Spending: Evaluate daily purchases, prioritize value, and align spending with long-term goals.

- Protecting assets: Assess risk, choose insurance for health and life, and safeguard property and other assets.

The American Institutes for Research stresses that financial literacy skills include the ability to find, understand, and use resources for informed decision-making. Use practical tools and targeted financial literacy resources to sharpen your knowledge, evaluate options, and plan for a secure future.

Mastering Your Monthly Budgeting Strategy

Simple rules can transform how you allocate income and track everyday spending. Start by listing take-home pay, fixed bills, and irregular expenses. Short, realistic steps make budgeting easier and help build financial literacy.

Consider the 50-30-20 rule: allocate 50% to needs, 30% to wants, and 20% to savings and investments. Alternatively, try the 80-20 approach and pay yourself first by setting aside 20% before other costs.

- Implementing 50-30-20 balances needs and wants while guaranteeing savings.

- Using 80-20 builds a habit of saving before spending on fixed items.

- Track spending each day to spot leaks and adjust quickly.

- Design a clear plan for personal finance to avoid debt and stress.

- Make informed decisions about monthly cash flow to reach long-term goals.

Small daily steps in tracking and simple allocation rules improve money control and strengthen financial decisions over time.

Building Wealth Through Consistent Savings

Automating deposits removes guesswork and helps you grow assets without daily effort. Simple systems make saving a habit and protect your money from impulse spending.

Automating Your Deposits

Open a dedicated savings account and set recurring transfers. This separates savings from checking and shields assets from accidental depletion.

Take advantage of employer matches by contributing enough to claim a 401(k) match. That match is free money and a fast route to increasing your investment balance.

- Automating deposits ensures you set aside funds each pay period no matter how busy your day is.

- Separate accounts reduce the temptation to use funds meant for the future.

- Consistent contributions build long-term financial literacy and help meet retirement goals.

View every dollar saved as a building block for the life you want. For practical tactics on steady savings, see this savings strategies guide.

Navigating the World of Personal Loans

When you need a loan for a car or education, smart research saves money and stress. Compare offers before you apply so monthly payments match your budget.

"Reviewing and comparing interest rates is essential before applying for any loan."

Borrow only what you can repay. Stick to amounts that fit current bills. That keeps debt manageable and protects credit.

- Compare interest and fees across lenders to find the best value.

- Account for total cost over time, not just the monthly payment.

- Use resources that explain loan terms so you avoid predatory offers.

- Treat debt management as a core part of financial literacy and personal finance.

Take time to weigh options and make decisions that protect long-term finance health. We provide tools and explanations so you never borrow more than necessary.

Essential Strategies for Real Estate Success

Good timing and basic checks turn property hunting into a practical step toward wealth. Start with clear goals and a savings plan that separates funds for a home from everyday money.

Property Ownership Basics

Understand ownership fundamentals. Know taxes, title issues, and maintenance costs before you buy. These basics shape long-term value and protect wealth.

Identifying Market Opportunities

Watch local trends and compare sale prices over time. Spend time analyzing neighborhoods, schools, and future development.

Set alerts and use simple tools to spot good deals early so your decisions match broader financial goals.

Evaluating Houses for Sale

When you evaluate a home, calculate true value and potential interest costs. Use a dedicated savings account or buckets in your account for down payment and closing costs.

- Understand the basics of property ownership as the first step toward building wealth.

- Use our tools to calculate value and long-term interest impact.

- Keep a dedicated savings account for the home so savings stay on track.

- Analyze market opportunities carefully to align real estate decisions with your plan.

For acquisition financing advice and practical options, see acquisition financing options at acquisition financing options.

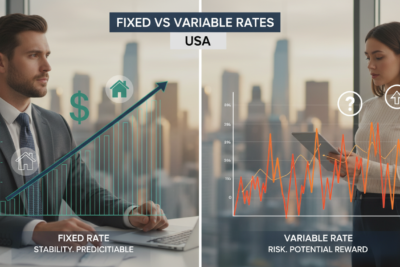

Finding the Right Mortgage for Your Future

Choosing the right loan shapes how quickly you build equity and reach long-term goals. Start by checking rates, terms, and the total cost of interest over time.

Use simple tools like a compound interest calculator to see how principal, rate, and term change monthly payments and total interest. These calculators help make complex numbers easy to compare.

Compare offers from several lenders and read fee schedules. Look beyond the headline rate; origination fees, points, and private mortgage insurance can change how much money leaves your account over years.

- Finding the right mortgage is a key step in financial literacy and we help make the process transparent.

- Our tools let you compare interest and loan terms so decisions support your home and future goals.

- Understand how different options affect cash flow so you pick a plan that fits budget and lifestyle.

Make informed decisions and secure a mortgage that aligns with long-term plans. Good choices now reduce stress later and strengthen overall literacy about money.

Protecting Your Assets with Proper Insurance

Insurance gives you a practical safety net so one emergency does not wipe out years of saving. Good coverage supports financial literacy and helps you make calm, clear decisions when events occur.

Life and Disability Coverage

Life insurance’s primary purpose is simple: provide financial protection for named beneficiaries if you die. A policy can replace income, cover final expenses, and protect kids or a partner.

Disability coverage protects your income if illness or injury keeps you from working. That protection preserves savings in your account and reduces the impact on monthly bills.

Health and Property Insurance

In the United States, many people get health coverage through an employer, but you can buy plans directly as well. Adequate health insurance reduces the financial impact of emergencies and serious illness.

Homeowners and auto policies guard your home and car from loss and liability. Review limits and deductibles so those risks do not drain your money.

- Protecting assets with life, health, and property insurance is a core part of solid personal finance.

- Proper coverage helps your literacy about money work in practice and keeps others safe.

- Keep accounts and policies updated so coverage matches changing needs and risk.

Managing Debt and Avoiding Financial Pitfalls

Debt can quietly erode progress if left unchecked, but simple steps can stop the slide. Start by tracking balances and reviewing how much interest you pay each month.

Keep credit card use tight: charge only what you can pay off monthly to avoid rising interest and protect your account. Pay more than the minimum on car or student loans when possible to cut total cost.

- Managing debt is a core part of financial literacy and helps you avoid high interest on cards and loans.

- Research all loan options and read terms carefully to spot predatory lending before you sign.

- Lower your debt-to-income ratio so unexpected expenses don’t derail long-term finance goals.

Use official guides and tools like financial literacy tools to compare offers and make better personal finance decisions. Small, steady changes to spending and payments build stronger money habits over time.

Tailored Financial Guidance for Diverse Communities

Communities face different barriers when learning basic money skills, and targeted help closes that gap. You need resources that match life experience, language, and legal or cultural context.

Resources for Underrepresented Groups

We provide tailored resources for veterans, immigrants, and communities of color so you can master basics like budgeting, debt, and savings.

The U.S. Federal Reserve highlights that many service members face trouble with debt management and emergency savings during transition. A TIAA Institute study shows African Americans often struggle most with insurance and risk concepts.

- Practical education: clear explanations of loans, account terms, and spending strategies.

- Targeted support: guides that address debt, health costs, and wealth building for specific groups.

- Accessible resources: links and toolkits designed for varied needs across the United States.

Ask questions and use vetted materials so you can make better decisions about money and long-term finance. For a federal resource directory on literacy, see the financial literacy resource directory.

Start with concise education and step-by-step help. Our beginner materials cover the basics and answer common questions so people from all backgrounds can improve wealth outcomes. Learn more with our beginner financial literacy basics guide.

"Targeted education reduces barriers and helps communities make stronger money choices."

Utilizing Professional Tools and Resources

Access to reliable tools turns confusing numbers into clear steps for smarter finance decisions.

Start with free planning tools from recognized sources. For example, Investor.gov (the U.S. SEC site) provides a compound interest calculator and other planning aids that help you model loans, savings, and investment growth.

Use these resources to test scenarios before you act. That practice improves your financial literacy and strengthens personal finance choices.

- Professional calculators clarify how interest changes outcomes over time.

- Vetted tools reduce guesswork and improve day-to-day money decisions.

- Targeted education and resources build skills and practical knowledge.

We connect you with quality resources and plain-language education so you can manage finances and maximize value over the long run.

Learn more about our mission and tools at About TipsLends.

Planning for Long Term Financial Goals

Mapping future goals into monthly tasks makes big financial aims feel achievable. Start with employer-sponsored retirement plans, such as a 401(k), and set a steady contribution schedule that fits your budget.

Planning for long-term goals like retirement requires discipline in savings and a clear view of investment options. Open a retirement account and track progress with simple milestones you can check each month.

- Break large goals into manageable steps and set target dates that match your life plans.

- Use our tools and resources to compare accounts and choose investments that suit your risk tolerance.

- Build financial literacy and skills so you make confident decisions about savings and investment choices.

Consistent contributions to a retirement account let time work in your favor. Small, regular deposits harness compound growth and help your money grow steadily toward long-term goals.

We provide clear education and practical tools that keep you motivated and on track as you pursue retirement and other life goals.

Overcoming Common Investment Challenges

Many investors struggle because they haven't matched risk limits to retirement timelines. Start by assessing how much risk you can accept without changing plans during market drops.

Understand risk tolerance and link it to goals like retirement and savings milestones. If time is long, you can accept more volatility; if retirement is near, shift toward lower-risk options.

Manage debt while you invest. High-interest debt often undermines wealth building, so pay down costly balances before boosting long-term investment contributions.

Learn common terms and use simple tools to compare interest, fees, and projected returns. Knowing basic concepts reduces anxiety and improves the quality of your decisions.

- Plan for volatility: keep a long-term allocation and rebalance on a schedule.

- Align options with retirement: choose vehicles that match timelines and tax needs.

- Protect value: reduce high-interest debt to free cash for consistent savings.

"Focus on a clear plan and steady contributions; time and discipline beat timing the market."

With clear education, practical tools, and consistent habits you can face common investment pitfalls and strengthen financial literacy while growing assets for the future.

Taking the Next Step Toward Your Financial Future

Begin with one practical habit today and expand it into a durable plan for housing, savings, and debt.

Taking the next step toward a secure future starts with a commitment to learn and apply simple principles. Small, steady moves change how you handle money and shape long-term financial decisions.

Explore our library of clear resources and tools that help make planning concrete. Review a practical financial reset and use a focused home buying checklist when preparing for purchase.

Every small, informed choice protects life goals and builds momentum. Take a strong, practical action today and keep building toward the future.

TipsLends Frequently Asked Questions

What are the basic principles of financial literacy I should learn first?

Start with income, budgeting, saving, and understanding interest. Learn how earning, spending, and saving interact. Know key terms like APR, compound interest, and emergency fund. These basics help you make better choices about debt, investments, and retirement.

How do I create a simple monthly budget that works?

Track your income and fixed expenses for one month, then categorize variable spending. Aim to allocate savings first, such as an emergency fund and retirement contributions. Use the 50/30/20 rule as a starting point and adjust it to match your goals and needs.

How much should I keep in an emergency savings account?

Aim for three to six months of living expenses if you have steady employment. If your income is unstable or you support others, target six to twelve months. Keep this money in a liquid, low-risk account like a high-yield savings account.

When should I consider taking a personal loan?

Consider a personal loan for consolidating high-interest debt, financing necessary medical costs, or covering urgent repairs when you lack savings. Compare interest rates, fees, and terms from banks, credit unions, and online lenders before borrowing.

How do I evaluate whether to rent or buy a home?

Compare total monthly costs, including mortgage, taxes, insurance, and maintenance, to rent. Factor in how long you plan to stay, local market trends, and your down payment ability. Use break-even calculators to estimate how many years you must live in the home to justify buying.

What should I look for when choosing a mortgage?

Compare fixed versus adjustable rates, loan terms, closing costs, and lender reputation. Check your credit score, gather preapproval offers, and understand private mortgage insurance requirements. Choose the option that fits your timeline and risk tolerance.

How can I manage and reduce high-interest debt effectively?

Use the debt avalanche method or the debt snowball method depending on what motivates you. Consider balance transfers, consolidation loans, or negotiating with creditors. Maintain on-time payments to protect your credit score.

How should I set long-term financial goals like retirement or buying a house?

Define a clear timeline, estimate costs, and prioritize goals by importance. Calculate required monthly savings using retirement and mortgage calculators. Increase contributions with raises and automate allocations to stay on track.

When should I seek professional financial advice?

Consult a certified financial planner or fiduciary when facing complex tax situations, estate planning, major life changes, or uncertain investment strategies. Ask for fee structures and check credentials before hiring an advisor.

What steps help protect credit and improve my score?

Pay bills on time, keep credit utilization low, avoid opening unnecessary accounts, and check your credit reports annually. Dispute inaccuracies promptly and maintain a healthy mix of credit types over time.

Need Financial Guidance?

Have questions about Real Estate, Mortgage, Loan, House for Sale, or Financial Guides? Visit our Contact Page and explore our educational resources designed to help you make informed financial decisions with confidence.

Go to Contact Page →