Credit Score Basics USA Made Simple for Your Financial Goals

Have you ever wondered why a three-digit number can shape your loan offers, interest rates, or rental chances?

You rely on clear information to manage money well. Understanding this system is the first step toward stronger financial choices and lower long-term costs.

Major bureaus like Experian, TransUnion, and Equifax collect your payment history and report it. A credit score is a three-digit value lenders use to judge risk and set terms.

This guide will explain how those numbers affect loan options and ways you can improve them. You’ll learn practical steps, from checking reports to managing balances, that help you qualify for better offers.

Want an official source to check reports or learn repair steps? See this practical guide for building and maintaining files and a clear overview of home affordability.

building and maintaining credit · home affordability basics

Table of Contents

- Understanding Credit Score Basics USA

- How Scoring Models Calculate Your Numbers

- The Role of Credit Bureaus and Reports

- Why Lenders Rely on Your Credit Profile

- Distinguishing Between FICO and VantageScore

- Factors That Influence Your Financial Standing

- What Defines a Good Credit Score

- Strategies to Build and Improve Your Credit

- Common Misconceptions About Credit Monitoring

- Navigating Credit Challenges Without a History

- Taking Control of Your Financial Future

- FAQ

Understanding Credit Score Basics USA

Lenders use a compact numeric snapshot to judge your borrowing risk and set loan terms. Most values fall within a 300 850 range, where higher numbers usually mean lower risk to the lender.

A good credit score is often 670 or above, and reaching that level can unlock lower interest rates and better offers. Your number changes as account activity is reported, so it reflects recent behavior as well as long-term patterns.

- Range helps lenders classify risk from high to low.

- Good credit opens more favorable financial options.

- Higher numbers tend to produce better loan terms.

| Range | Typical Meaning | Why it matters to lenders |

|---|---|---|

| 300–579 | Higher risk | Limited approvals; higher rates |

| 580–669 | Fair | Some approvals; average terms |

| 670–739 | Good | Stronger approvals; better pricing |

| 740–850 | Very good to excellent | Best rates and offers |

To dig deeper into how numbers are calculated and reported, see understanding credit scores.

How Scoring Models Calculate Your Numbers

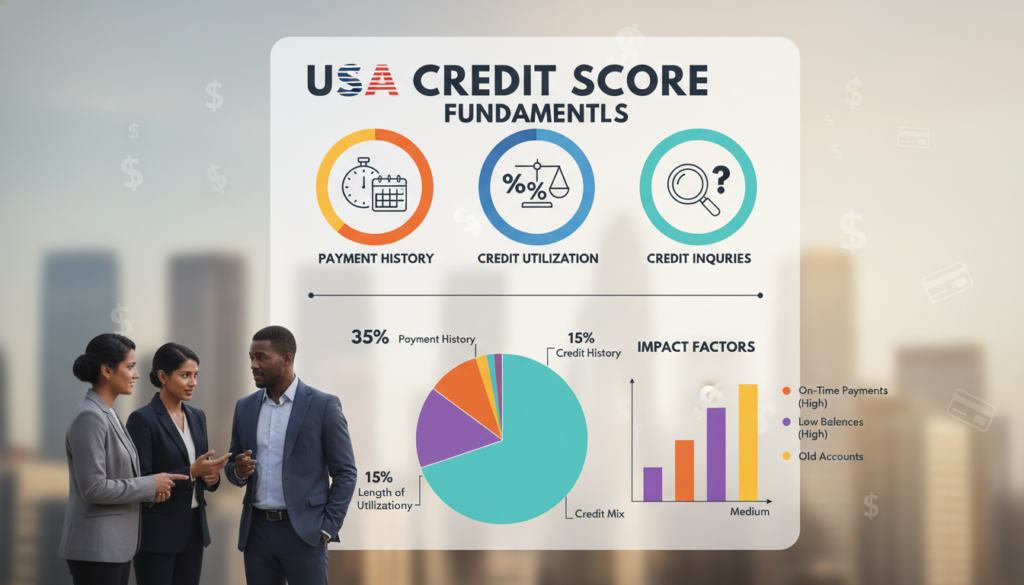

Behind every numeric rating are rules that interpret your payments, balances, and account types. Models read the data in your report and weight each factor to produce a three-digit result lenders use to assess risk.

Payment History Impact

Payment history drives about 35% of a FICO result. Scoring models check if you pay on time and how often you miss deadlines.

Even one late payment can move your profile toward higher risk. Keeping timely payments is the most reliable way to protect and improve your standing.

Credit Utilization Ratios

Utilization is the share of your revolving limits you actually use. It explains roughly 30% of many models' calculations.

Use low balances relative to limits to reduce risk quickly. This is one of the fastest levers to improve your short-term position.

"Scoring models transform account activity and report data into an objective measure lenders rely on when pricing loans."

- Length of history shows how long you manage accounts.

- A mix of auto, mortgage, and revolving accounts can help overall ratings.

- Applying for new credit creates recent activity that models monitor.

| Factor | Typical Weight | Why it matters |

|---|---|---|

| Payment history | ~35% | Shows on-time repayment and risk of default |

| Utilization | ~30% | Measures current debt vs available limits |

| Length & mix of accounts | ~20% | Provides depth and diversity of handling different loans |

| Recent activity | ~15% | Reveals new credit requests and short-term changes |

For a deeper breakdown of what goes into a FICO calculation, see what's in your FICO. If you're preparing to buy a home, learn how these elements affect mortgage readiness at home buying tips.

The Role of Credit Bureaus and Reports

A handful of nationwide bureaus aggregate your account activity and public records into formal reports.

Experian, TransUnion, and Equifax collect the raw data lenders send them. They compile that data into detailed reports that show your payment history, accounts, and public filings.

You have the right to check reports from each bureau to confirm the information is accurate. If you spot an error, you can dispute it directly with the agency to protect your standing.

"These agencies store your history; scoring models then use that data to calculate how risky you appear to lenders."

- The three major bureaus maintain the files lenders consult when evaluating you.

- Different lenders may report to different bureaus, so reports can vary.

- Regularly reviewing reports helps you spot fraud and correct mistakes quickly.

| Agency | What it stores | Why it matters |

|---|---|---|

| Experian | Accounts, payments, public records | Feeds models that produce your scores used by lenders |

| TransUnion | Recent activity and account status | Shows current risk and recent inquiries |

| Equifax | Account balances and collections | Helps verify your financial history for loans |

Why Lenders Rely on Your Credit Profile

Lenders turn your financial file into a quick risk report when you apply for loans or new accounts. This helps them act fast and treat applicants consistently.

How Lenders Assess Risk

Your credit score and report give lenders a snapshot of payment patterns, balances, and account types. They use that information to forecast how likely you are to repay.

Automated checks speed decisions for credit card approvals, mortgage offers, and auto financing. A higher credit score can lower the rate you pay over time.

- Lenders review your profile to judge the chance you will repay on time and set terms accordingly.

- When you apply for a credit card, issuers check the score to approve or set limits.

- Mortgage lenders use your history to price home loans and affect your monthly payment.

- Auto lenders evaluate your file to offer competitive financing for vehicles.

- Strong standing often wins higher limits on revolving accounts and better loan rates.

- Because lenders rely on consistent data from reports, keeping your information accurate matters.

"By maintaining a strong profile, you signal low risk and access more favorable offers."

For more on what lenders look for, see what is a good credit score. If you are preparing to buy a home, review practical steps at home buying guide.

Distinguishing Between FICO and VantageScore

Two companies dominate the market for consumer scoring models. Each reads the same reports but applies different rules to produce a three-digit result.

FICO Scoring Models

FICO has been the industry standard since 1989. Versions such as FICO Score 8 are widely used by lenders for general lending decisions.

There are also specialized FICO variants that lenders may pick for auto or mortgage underwriting.

VantageScore Variations

VantageScore offers alternative models like VantageScore 4.0 that can score more consumers with limited history.

These models sometimes weigh recent data or certain account types differently than legacy FICO models.

Why Scores Differ

Your number can differ because each company uses unique formulas and weights for report data. Hard inquiries, payment timing, and types of accounts may be treated differently.

Models update periodically, so a change in behavior or a new model release can shift results even if your activity is steady.

| Aspect | FICO | VantageScore |

|---|---|---|

| Common model example | FICO Score 8 | VantageScore 4.0 |

| Typical range | 300–850 | 300–850 |

| Treatment of thin files | May not score limited histories | Often scores more consumers |

| Lender usage | Widely used by banks and mortgage underwriters | Increasingly used by lenders and services |

Understanding these differences helps you interpret varying numbers from different sources. For more detail on how the two systems compare, see the Experian comparison of FICO and.

Factors That Influence Your Financial Standing

Several clear factors shape how lenders view your financial reliability over time.

Payment history leads the list because it shows whether you pay on time. Missed payments move your rating toward higher risk quickly.

The share of available revolving limits you use called utilization matters next. Lower balances compared with limits improve short-term standing and help the overall rating.

The length of your history tells lenders how long you’ve managed accounts. Older accounts often strengthen your profile.

- New inquiries from applying for new credit can lower results temporarily.

- A mix of installment and revolving accounts shows varied experience with loans and cards.

- Scoring models read the data in your reports to calculate final numbers.

Credit bureaus supply the raw information that models use. To learn which items most affect outcomes, read what affects your credit scores.

"Focus on on-time payments and lower balances to improve your financial standing over time."

What Defines a Good Credit Score

Small shifts in your financial profile can translate into big savings over time.

A good credit score is commonly viewed as a range where lenders see lower risk. Many mortgage underwriters treat a FICO value of 670 or higher as the line that opens stronger terms.

Beyond the number, your payment history and how you use revolving limits matter most. These factors shape approvals, interest rates, and available products such as a new credit card or mortgage offer.

Impact on Mortgage and Auto Loans

When your standing sits in the 670–739 band, you’re more likely to receive favorable mortgage pricing. Auto loans follow the same pattern: higher standing yields lower rates and better loan types.

- Approval odds improve when lenders view you as low risk.

- Interest savings grow even with modest jumps inside the 300 850 range.

- Limits and loan choices expand as your history shows steady payments.

| Range | Typical Outcome | Why it matters |

|---|---|---|

| 670–739 | Good — better loan offers | Lower rates for mortgage and auto loans |

| 740–850 | Very good to excellent | Best pricing and top lender access |

| 300–669 | Fair to high risk | Higher cost and stricter underwriting |

"Higher standing signals lower risk, which often reduces long-term borrowing costs."

Strategies to Build and Improve Your Credit

Practical habits you use every month often matter more than big moves when improving your financial standing.

Pay every bill on time. Your payment history has the biggest effect. Late marks can remain on a credit report for up to seven years, so timeliness matters.

Keep revolving balances low. Paying a credit card bill early can lower the utilization lenders see and help your score quickly.

Check your reports regularly. When you review credit reports, you can spot errors and dispute inaccurate information that hurts your history.

- Set automatic payments for all accounts to protect payment history.

- Open a secured card if you are new credit to start a reliable record.

- Avoid many applications at once; new credit inquiries can lower short-term standing.

- Manage credit accounts responsibly to show lenders you handle revolving debt over time.

"Building a strong profile is gradual and rewards consistent, positive habits and careful debt management."

Common Misconceptions About Credit Monitoring

Many people worry that checking their own financial file will harm future loan offers. That fear is a myth.

Viewing your own report is a soft inquiry. When you check on your numbers, lenders do not see those checks. Soft inquiries never lower your standing.

You can review your cards and accounts as often as you like. Frequent monitoring helps you spot errors, fraud, or missing payments fast.

- Checking your own score or report does not hurt your approval odds.

- Your report does not include income details, so earnings don’t affect scoring directly.

- Monitoring services use soft inquiries that lenders never view.

"Regular checks give you valuable information without risking your number."

Trust official sources and simple facts. If you want a concise guide on myths, read five misconceptions about credit scores. Stay proactive checking often protects your financial health.

Beginning without recorded accounts doesn’t mean you can’t show lenders you are low risk. There are practical tools that let you build a reliable financial profile over time.

Becoming an authorized user on a family member’s card can add positive payment data to your report. This gives scoring models the activity they need to generate a score when you have no accounts of your own.

Choose an account with steady on-time payments and low balances so the added history helps rather than harms your standing.

Credit Builder Tools

Credit builder loans and secured cards are designed for people starting out. A builder loan records monthly payments to a reporting agency while you pay into a held account.

Secured cards require a cash deposit and function like regular cards. Regular, small purchases and timely payments will help improve credit and speed up the process.

- Ask to add eligible utility or phone bills to your reports to register consistent payments.

- Start with one or two small accounts so scoring models collect the needed data.

- Monitor your credit reports to confirm new accounts appear and are reported by the credit bureaus.

"It takes time to build a solid financial history, but these tools let you show reliable behavior faster."

Taking Control of Your Financial Future

Small, steady choices today can shape the borrowing opportunities you see tomorrow.

Achieving a good credit score is one powerful way to take control of your financial future and reach long‑term goals.

By practicing steady habits timely payments, low balances, and regular report checks you stay ready for major purchases like a home or a car.

Your score reflects your financial journey and can improve with time. Stay informed so you make smarter decisions and avoid setbacks.

You have the tools and knowledge to build a strong foundation. Start now: review your reports and take small, consistent steps that lead to lasting success.

FAQ

What is a credit score and why does it matter?

A credit score helps lenders evaluate borrowing risk and influences approvals, rates, and available credit limits.

How do payment history and on-time payments affect my number?

Consistent on-time payments improve financial standing, while missed or late payments can significantly reduce scores.

What is credit utilization and how should you manage it?

Credit utilization compares balances to limits, and lower percentages usually indicate healthier financial management habits.

How often do credit bureaus update my report?

Most lenders report account activity monthly, though updates may take several weeks to appear across bureaus.

Why do lenders review your profile differently?

Each lender uses different scoring models, internal criteria, and risk standards when evaluating financial applications.

What are the main differences between FICO and VantageScore?

Both scoring systems analyze similar factors but use different algorithms and weighting methods for evaluations.

Why can your numbers differ between models or bureaus?

Variations occur because bureaus receive different updates and scoring models calculate risk differently.

Which factors most influence your financial standing?

Payment history, utilization, account age, credit mix, and recent inquiries strongly impact overall creditworthiness.

What is considered a good score and how does it affect mortgage or auto loans?

Higher scores generally qualify for lower rates, better loan terms, and improved financing opportunities.

How can you build or improve your rating quickly and safely?

Pay bills consistently, lower balances, avoid excessive inquiries, and maintain older accounts responsibly over time.

What are common myths about monitoring your reports?

Checking your own reports does not damage scores, and monitoring tools help identify fraud and reporting errors.

How do you build a record if you have little or no history?

Secured cards, authorized user accounts, and credit-builder loans help establish positive payment records gradually.

What are authorized user status and credit-builder tools?

Authorized user access and secured financial products help individuals create stronger borrowing histories safely.

How often should you check your reports and what should you look for?

Review reports regularly for inaccuracies, unfamiliar accounts, balance errors, and signs of identity theft.

Can paying off collections immediately restore your rating?

Settling collections helps gradually, though negative reporting may remain visible for a period after repayment.

How do new accounts and hard inquiries affect you?

Frequent applications and hard inquiries may temporarily reduce scores and signal higher lending risk.

When should you consider professional help for repair or counseling?

Seek professional assistance when struggling with overwhelming debt, repeated delinquencies, or serious reporting disputes.

If you want to know other articles similar to Credit Score Basics USA Made Simple for Your Financial Goals You can visit the category Credit.

How Lenders Evaluate Credit and What You Should Know

Credit Report Explained USA Tips to Understand Yours

Improve Credit Score USA with These Simple Tips

How Credit Score Works USA and Why It Matters to You

Key Factors Affecting Credit Score for Your Financial Health

Best Property Search Tips USA for Your Home Buying Journey

Leave a Reply

VISIT THESE INTERESTING ARTICLES📚