Your Guide to Types of Mortgages USA and How They Work

Wonder which home loan truly fits your budget and plans? You might assume a single route will save you money. But your credit, savings and time horizon shape which mortgage and lender make sense.

In this short guide you’ll learn the main mortgage loan choices conventional, government-backed, jumbo, fixed rate and adjustable-rate mortgages and how each affects your monthly payment and long-term costs.

Before you sign, evaluate your income, credit scores and down payment. Factor in insurance, private mortgage insurance and closing costs so your monthly payments match your life plans.

Start by comparing lenders and loan estimates. For a deeper breakdown of specific options, see a quick primer on mortgage types and features and a clear fixed-versus-variable comparison at fixed vs. variable mortgage.

Table of Contents

- Understanding the Landscape of Types of Mortgages USA

- Conventional Loans for Traditional Homebuyers

- Government-Backed Loan Programs

- Fixed-Rate Versus Adjustable-Rate Options

- Specialized Financing for Unique Property Needs

- Second Mortgages and Home Equity Solutions

- Factors Influencing Your Mortgage Eligibility

- Strategic Considerations for Your Financial Future

- Final Steps Toward Securing Your Ideal Home Loan

Understanding the Landscape of Types of Mortgages USA

Choosing the right home loan starts with a clear look at your credit score, income and how long you plan to stay in the property.

Your score is a primary filter lenders use in the current market. It affects which loan options you can get and the interest rate you’ll pay.

When you compare a mortgage loan, review how your income and debts change your borrowing power. Also check mortgage insurance rules and expected monthly payment.

Many homeowners find the best choice depends on personal finances and years you expect to keep the home. A broker can help match your profile to suitable loan types and lenders.

- Assess credit and income first.

- Estimate total costs, including mortgage insurance and closing fees.

- Use professional guidance for complex situations.

"Understand your credit and timeline before you lock a rate; it saves money over the long run."

| Factor | What to Check | Why It Matters |

|---|---|---|

| Credit score | Recent report and score | Determines eligibility and interest rate |

| Income & debt | Pay stubs, DTI ratio | Sets loan amount you can afford |

| Insurance & fees | Mortgage insurance, closing costs | Affects monthly payment and upfront costs |

| Time horizon | Years you plan to stay | Guides fixed vs. adjustable decisions |

For a clear summary of different loan options, review this guide to loan options before you apply.

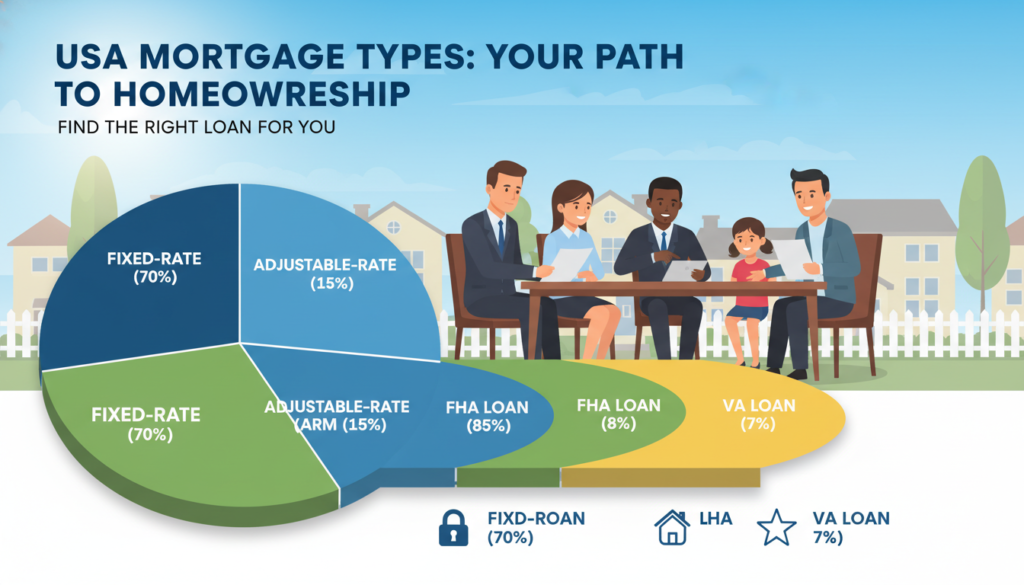

Conventional Loans for Traditional Homebuyers

Conventional loans are popular when you want predictable payments and flexible terms. You’ll find them widely offered by private lenders and they suit buyers with steady income and a solid credit score.

Conforming Loans

Conforming loans follow limits set by the Federal Housing Finance Agency. For 2025, the single-family limit is $806,500 in most markets.

You generally need a credit score of at least 620 and thorough documentation of income and assets to qualify.

Non-Conforming and Jumbo Loans

Non-conforming loans, including jumbo options, cover purchases that exceed conforming caps. These loans often require higher down payments and more proof of income.

If you put less than 20% down, expect private mortgage insurance until you build equity. Many homeowners choose conventional loans for the flexibility they give investors compared to government programs.

"Choose the right type of conventional loan to manage your monthly payment and interest over the life of the mortgage."

Government-Backed Loan Programs

Government-backed programs can open doors when your savings or credit make a conventional loan hard to qualify for.

These options are designed to expand access to home ownership. They each have unique rules on credit, down payment, insurance and property location. Below are the main programs and what they offer.

FHA Loan Benefits

FHA loans are insured by the Federal Housing Administration and favor borrowers with lower credit scores and limited savings.

You can qualify with a credit score as low as 580 and a 3.5% down payment. Expect mortgage insurance premiums and standard closing costs.

VA Loan Advantages

VA loans are guaranteed by the U.S. Department of Veterans Affairs for eligible service members and veterans.

They often require no down payment and charge competitive interest rates. You will still review closing costs and any required fees with approved lenders.

USDA Rural Development Loans

USDA loans are backed by the Department of Agriculture and support home purchases in qualifying rural areas.

These loans target moderate-income borrowers and can offer no down payment. You must confirm property eligibility and income limits with an approved lender.

- Each program may require mortgage insurance or insurance premiums.

- Compare costs, rates, and eligibility before you apply.

- Contact approved lenders to verify your income and credit profiles.

"Government loan programs can lower upfront costs and stretch your buying power when used correctly."

| Program | Key Benefit | Common Costs |

|---|---|---|

| FHA | Low credit threshold (580) and 3.5% down | Mortgage insurance premiums, closing costs |

| VA | No down payment for eligible veterans | VA funding fee (may apply), closing costs |

| USDA | No down payment for qualifying rural properties | Upfront guarantee fee, closing costs |

For a quick comparison of specific loan features and next steps, see this detailed guide to loan options.

Fixed-Rate Versus Adjustable-Rate Options

Deciding between a steady fixed rate and a shifting adjustable option shapes how your monthly payment behaves over years.

A fixed-rate mortgage keeps the same interest rate for the life of the loan. That means your principal and interest portion of each payment stays predictable, which helps when you plan a long-term budget.

An adjustable-rate option, like a 5/1 ARM, offers a fixed interest for the first five years and then adjusts annually. That initial lower rate can reduce payments early, making it attractive if you expect to move or refinance within a few years.

Weigh your comfort with risk. ARM payments can rise if market rates climb. Check the lifetime adjustment cap to know the maximum your interest rate can change over the life loan.

- Stability: Fixed loans protect you from market swings and ease long-term planning.

- Short-term savings: Adjustable-rate loans often start lower and can save money if you sell or refinance before adjustments.

- Qualification factors: Your credit score and income affect the interest rates lenders offer for both options.

"Always review the mortgage terms so you understand how your monthly payments might change with an adjustable-rate loan."

For a clear, side-by-side comparison, review this guide to ARM vs. fixed-rate choices before you commit.

Specialized Financing for Unique Property Needs

When you're building, renovating, or buying with an unusual income profile, tailored loan solutions can bridge the gap.

Construction and renovation loans let you fund a new build or a major remodel. These loans often require a higher down payment and stage-based draws while work is underway.

Expect inspections and tightened timelines. Lenders monitor progress before releasing funds. Your payment may change once the loan converts to a standard mortgage after construction ends.

Physician and Portfolio Loans

Physician loans target medical professionals who carry heavy student debt but strong future income. Some offer low or no down payment and can waive private mortgage insurance.

Portfolio loans are kept on a lender's books and can be more flexible for unique borrowers or properties. They may accept nonstandard income documentation or higher loan sizes.

- Credit and income reviews differ from standard underwriting.

- Specialized options can carry slightly higher interest rates or specific fees.

- Work with a lender to compare full costs and payment scenarios.

"Specialized financing can unlock projects and purchases that standard loan paths won't support."

| Loan Type | Key Benefit | Common Requirement |

|---|---|---|

| Construction / Renovation | Funds building or major remodels | Higher down payment, progress inspections |

| Physician | Low/no down payment, flexible debt treatment | Proof of medical employment or contract |

| Portfolio | Flexible underwriting for unique cases | Lender-held loan; may have higher rate |

Before you apply, discuss your property needs with a loan officer and review long-term costs. For a deeper look at loan options, see this detailed loan guide.

Second Mortgages and Home Equity Solutions

Accessing home equity gives you choices: a one-time lump sum, a revolving credit line, or a reverse option for older homeowners.

A second mortgage lets you tap the equity you have built to fund major expenses or consolidate debt. A home equity loan delivers a lump sum with a fixed rate and regular payments.

A HELOC works like a credit card: it’s a revolving credit line that you draw against as needed. That flexibility can help with ongoing projects or cash flow needs.

- Second mortgage: lump-sum cash, fixed payment schedule.

- HELOC: flexible draws, variable rates, pay interest only on what you use.

- Reverse mortgage: for homeowners 62 and older; provides tax-free payments based on equity.

Remember: these loans are secured by your property. Missing monthly payments or failing to pay property taxes and homeowners insurance can risk foreclosure.

"Always consult a financial advisor to see how a second mortgage or reverse mortgage affects your long-term financial life."

For a clear comparison and next steps, review a guide to second mortgage vs home equity loan and basic mortgage loan details at mortgage loan basics.

Factors Influencing Your Mortgage Eligibility

Lenders weigh several financial signals when they decide if you qualify for a home loan.

Your credit score is one of the top measures they check. A higher score shows you manage credit well and may help you secure a lower interest rate.

Next, lenders calculate your debt-to-income (DTI) ratio. This shows whether your income covers a new mortgage payment plus existing debts.

A clear credit history and documented income speed approval. Gather pay stubs, tax returns, bank statements, and asset records before you apply.

The current market and the type of property you buy can change underwriting rules. Some properties or loan programs require stricter checks or higher reserves.

- Maintain steady income and trim revolving debt before you apply.

- Check your credit report for errors and fix them early.

- Prepare full documentation to avoid surprises at closing.

"By preparing your finances and documentation, you improve your chances to get better loan terms."

| Factor | What lenders review | How it affects your loan |

|---|---|---|

| Credit score | Credit reports, payment history | Impacts interest rate and offers |

| DTI ratio | Monthly debts vs. income | Determines acceptable payment level |

| Income & documentation | Pay stubs, tax returns, assets | Supports loan amount and approval |

Want to understand how interest might change your monthly payment? Read this guide to mortgage interest explained for practical examples.

Strategic Considerations for Your Financial Future

Match the mortgage you choose to a clear exit plan and income forecast.

Plan how long you will stay in your home. That timeline guides whether a fixed rate or an adjustable option fits you.

Evaluate total monthly payments against likely income growth. This helps you avoid payment shock and keeps your budget stable.

Keep your credit in good standing. A strong score lets you access better loan rates and makes future refinances simpler.

"Map your loan choice to your long-term exit strategy."

- Consider how rising interest rates affect refinancing options.

- Choose a loan that matches your retirement and investment plans.

- Borrowers who plan early usually save significant money over time.

| Factor | Why it matters | Action |

|---|---|---|

| Time horizon | Affects whether a fixed or adjustable rate saves money | Pick loan term to match years you plan to stay |

| Monthly payments | Determines cash flow and affordability | Run scenarios for income growth and shocks |

| Credit & refinance options | Impacts rates and ability to lower interest later | Maintain credit; plan refinance triggers |

For practical next steps when preparing to buy, see this preparing to buy guide.

Final Steps Toward Securing Your Ideal Home Loan

Finish strong by verifying loan quotes and preparing documents so you can lock a competitive rate.

Start by comparing offers from multiple lenders to find the best interest rates and suitable loan types. Check sample fees and service terms, then use a trusted checklist to stay organized. For step-by-step guidance, see this apply-for-mortgage guide.

Confirm your credit score meets the program requirements and review your income and planned monthly payments. Make sure the mortgage fits your budget before you commit.

Once you pick a loan, work closely with your lender to finish the application, provide documents quickly, and lock the rate. The right mortgage is a tool to help you reach homeownership while protecting long-term financial health.

If you want to know other articles similar to Your Guide to Types of Mortgages USA and How They Work You can visit the category Mortgage.

Choosing the Right Mortgage A Guide for Your Home Loan

Step by Step Home Buying Process USA Made Simple

Loan Approval Process Explained for Your Home Loan

Loan Preparation Checklist USA Every Borrower Should Use

Financial Preparation Checklist for Loans Made Easy

Documents Needed for Mortgage Checklist You Can Use

Leave a Reply

VISIT THESE INTERESTING ARTICLES📚